Deferred Tax On Mat Credit

Managerial Remuneration Under The Companies Act 2013 Managerial Persons Covered Taxation Acting Management Central Government

Fin 534 Midterm Exam 1 Which Of The Following Statements Is Correct 2 You Are Considering Two Equally Risky Annuities Each Of Whic Final Exams Exam Midterm

Deferred Tax Liability Accounting Double Entry Bookkeeping

Deferred Tax Asset Journal Entry How To Recognize

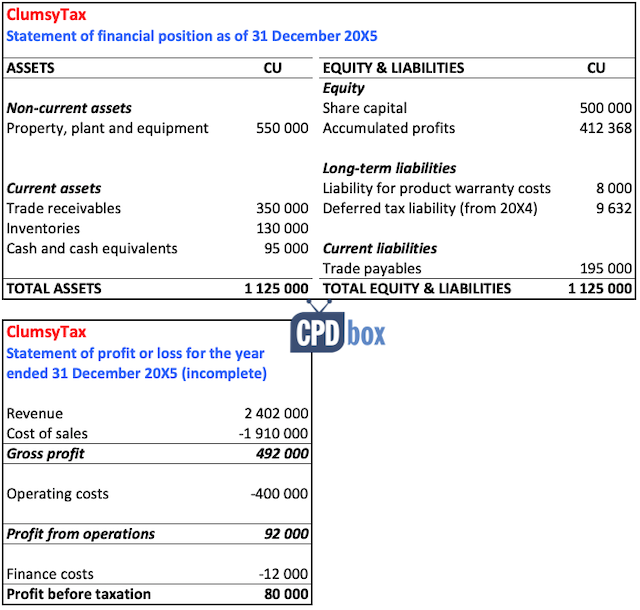

Tax Reconciliation Under Ias 12 Example Ifrsbox Making Ifrs Easy

Individual Income Tax Faq Alabama Department Of Revenue

2 when ur income is less as per income tax act than the income as per companies act deferred tax liability arises.

Deferred tax on mat credit. Corporate bookkeepers debit and credit deferred tax specific accounts depending on the transaction. Minimum alternative tax is payable under the income tax act. Section 115jb levies minimum alternate tax mat at 10 of book profits plus surcharge and cess thereon if such tax is higher than the tax payable under the normal provisions of the act. Deferred taxes result from temporary differences between the book value of a company s assets and liabilities and their tax worth.

Whether mat credit is a deferred tax asset 4. Mat a brief introduction. An issue has been raised whether the mat credit can be considered as a deferred tax asset within the meaning of accounting standard as 22 accounting for taxes on income issued by the institute of chartered accountants of india. In this context the following definitions given in as 22 are noted.

Under accounting standard as 22 discussed above though mat credit is not a deferred tax asset an expectation regarding future economic benefit arises in the form of the adjustment of the future income tax liability that arises within a specified time period. 11 april 2008 1 when ur income is more as per income tax act than the income as per companies act deferred tax asset arises. The treatment of deferred tax charge in determining the tax liability under the special provisions of section 115jb of the income tax act is one such case. Mat credit is not a deferred tax asset as per as 22 on accounting for taxes on income issued by icai deferred tax liability or deferred tax asset arises on account of timing differences i e.

Whether mat credit can be considered as a deferred tax asset per as 22. 3 for provisions of mat refer sec 115jb of the it act 1961. The differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods. In most countries if you made a loss last year you can pay less tax this year on your profits.

The concept of mat was introduced to target those companies that make huge profits and pay the dividend to their shareholders but pay no minimal tax under the normal provisions of the income tax act by taking advantage of the various deductions and exemptions allowed under the act. In the bucket marked deferred tax are timing differences tax losses and tax credits. Mat does not give rise to any difference between book income and taxable income. They also may come from timing differences between the recognition of gains and losses in the.

2 whether mat credit can be considered as an asset.

Significant Accounting Policies Mindtree

I Keep Hearing Invoices Business Taxes Finances Divorce Accounting Accountingservices Taxse In 2020 Business Valuation Accounting Services Forensic Accounting

What Is The Applicable Minimum Alternate Tax Mat Rate For Ay 2020 21

Second Thoughts Borrowing Money From Family Fincon Bloggers The Borrowers Money Personal Finance

How To Prepare W 2s For Church Employees Including Ministers Church Law Tax

Good Things To Accrue Good Things To Defer Funny Accountant Etsy Accounting Jobs Accounting Humor Funny Accountant

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Pdf What Problems And Opportunities Are Created By Tax Havens

Http Www Uml Edu Docs How To Read Paystub Tcm18 86893 Pdf

Print Of Queen Elizabeth I By Hilliard Etsy In 2020 Fashion Elizabeth I Elizabethan Dress

Debt Schedule Timing Of Repayment Interest And Debt Balances

Deferred Tax Assets Explained Youtube

All About Deferred Tax And Its Entry In Books

Https Www Sanantonio Gov Portals 0 Files Nhsd Tif Agreements T30 Peanutfactory Cchip Pdf

Https Www2 Deloitte Com Content Dam Deloitte Sg Documents Tax Sg Tax 2019 Asia Pacific Financial Services Tax Conference Slides Hong Kong Pdf

Income Tax Provision Entry In Tally Provision For Income Tax Entry In Tally Part 1 Youtube

India Glycols Ltd Fundamental Analysis Dr Vijay Malik

Https Aaml Org Resource Collection 3bdedfa9 B18b 4c53 B875 2cf630ddad9c Wilder Pdf

1

Https Www2 Deloitte Com Content Dam Deloitte Ch Documents Audit Ch En Audit Benchmarking Auditors Report Pdf

Good Neighbor Relief Returning 2 Billion Dividend

/GettyImages-1174783743-8a784400ff9e4fa79fbfffd9fc789a79.jpg)

Are Roth 401 K Plans Matched By Employers

Http Www Bancoindia Com Wp Content Uploads 2018 05 Afrbpil2018 Pdf

Https Assets Kpmg Content Dam Kpmg In Pdf 2020 01 Chapter 1 Aau Tax Ordinance Pdf

Https Www Hollywoodfl Org Documentcenter View 16435 Fy 2020 Proposed Budget

:max_bytes(150000):strip_icc()/buyback-f91333fa039d4d79ab430c65fc753e11.jpg)

Loss Carryforward Definition

Covid19 Tax Resource Page Jmf

Rentals Leases How Does Sales Tax Apply To Them Sales Tax Institute

Direct Indirect Expenses Definition Examples Video Lesson Transcript Study Com

Http Www Broward Org Accounting Documents 2018cafr Pdf

Monthly Gaap Bulletin November 2019 By Grant Thornton In India

Gap 101 4 Payroll Deductions Accounting Duke

Live In Nh But Work In Ma What To Know About Your State Tax Returns Milestone Financial Planning

Current Portion Of Long Term Debt Cpltd Definition

Filing An Alabama State Tax Return Things To Know Credit Karma Tax

Https Www Singtel Com Content Dam Singtel Investorrelations Stockexchange 2020 Balrelease 20200730 Pdf

/GettyImages-1191254826-9a51e4759f2e43af8b521031bcf24f43.jpg)

Non Operating Asset Definition

Why You May Owe Taxes At The End Of Your Maternity Leave Vancouver Sun

Nigeria Finance Act 2019 Changes Bdo

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Dbriefs India 20taxation 20laws 20 Amendment 20ordinance 202019 3 20october 202019 Pdf

Index Of Wp Content Uploads 2019 05