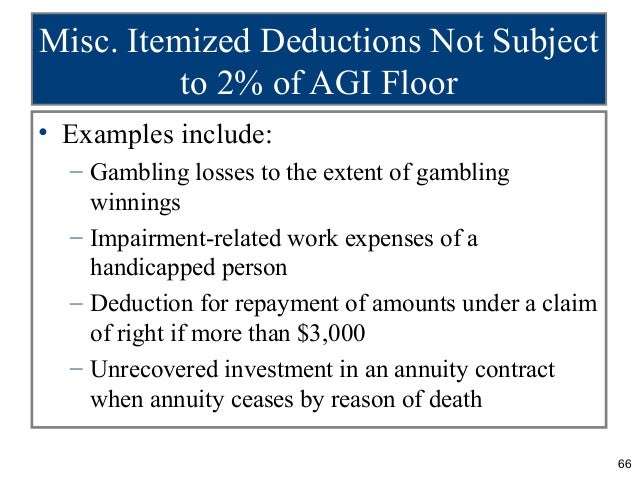

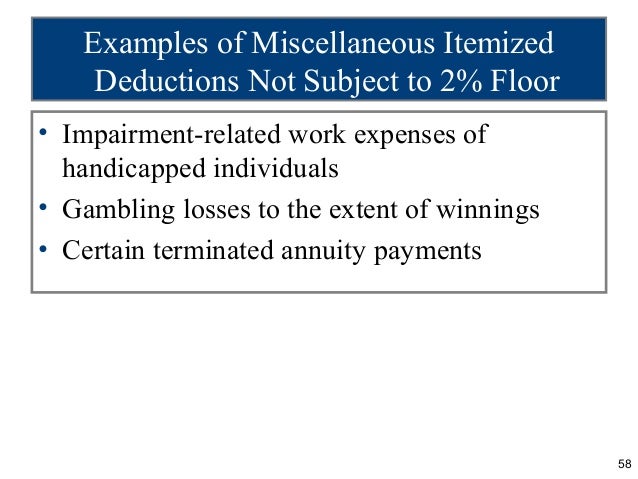

Deductions Not Subject To 2 Floor

Form W 11 Number 11 11 Common Mistakes Everyone Makes In Form W 11 Number 11 Form W 11 Number 11 11 Common Mistakes Everyone Makes In For How To Get Money Irs

To Know The Tax Benefits Provided To First Time Home Buyers Watch Out Image Below To Grab These Benefits Just Call Out 8852 Finance Loans Loan Investing

Vol 01 Chapter 10 2015

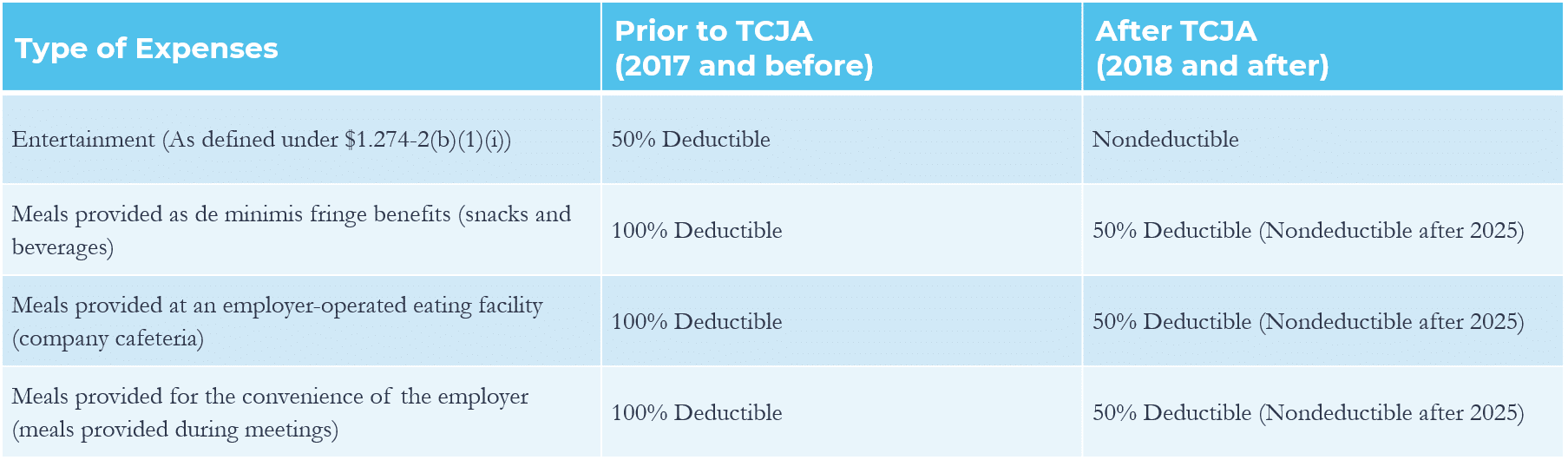

Navigating The New Meals And Entertainment Deductions Under Tcja Grf Cpas Advisors

Check Out All The Things Educators Can Deduct From Their Taxes Save Those Hard Earned Dollars Teache Teacher Tax Deductions First Year Teaching Teacher Info

Potential Tax Benefits With Images Disabled Children Williams Syndrome Parenting

A type of expenses subject to the floor 1 in general.

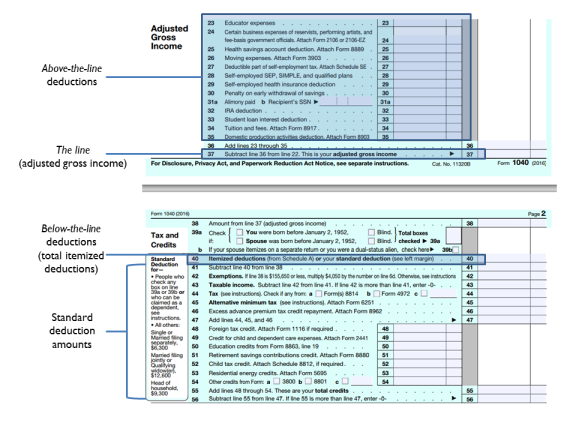

Deductions not subject to 2 floor. This code has been deleted. These porfolio deductions are not subject to the 2 floor. To figure the amount of your allowable deduction for these expenses the irs provides a section on schedule a job expenses and certain miscellaneous deductions. You can still claim certain expenses as itemized deductions on schedule a form 1040 1040 sr or 1040 nr or as an adjustment to income on form 1040 or 1040 sr.

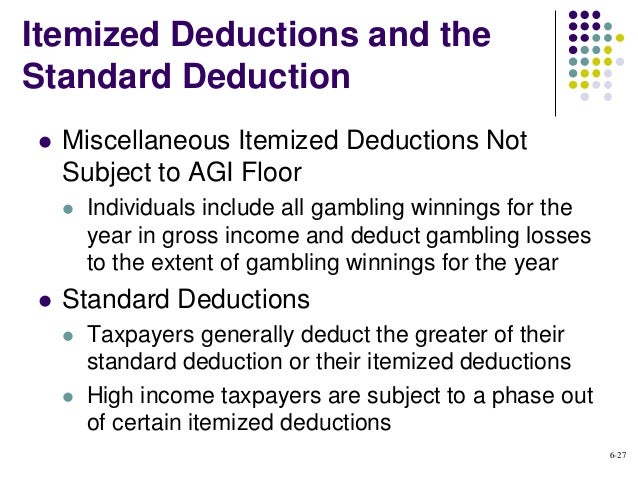

This publication covers the following topics. Miscellaneous itemized deductions subject to the 2 floor aren t deductible for tax years 2018 through 2025. Deductions in excess of income in the final year of a trust or estate pass through to beneficiaries as miscellaneous itemized deductions even if the expenses. There are two types of miscellaneous deductions.

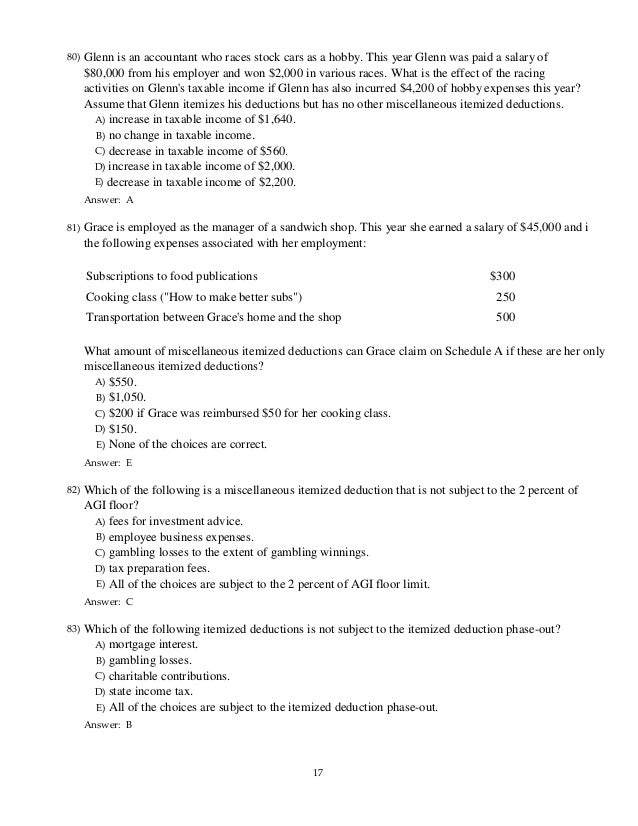

The irs issued final regulations on the controversial question of which costs incurred by trusts and estates are subject to the 2 floor on miscellaneous deductions under sec. You cannot simply reduce your gambling winnings by your gambling losses and report the difference. Miscellaneous deductions are deductions that do not fit into other categories of the tax code. Thus you should not need to make additional entries as other current year decreases.

In prior years amounts subject to the 2 floor on line 13 of sch k 1 would have been coded with a k. 1 deductions subject to the 2 limit these deductions allow you to deduct only the amount of expense that is over 2 of your adjusted gross income or agi. These losses are not subject to the 2 limit on miscellaneous itemized deductions. With respect to individuals section 67 disallows deductions for miscellaneous itemized deductions as defined in paragraph b of this section in computing taxable income i e so called below the line deductions to the extent that such otherwise allowable deductions do not exceed 2 percent of the individual s adjusted gross.

Shall prescribe regulations which prohibit the indirect deduction through pass thru entities of amounts which are not allowable as a deduction if paid or incurred directly by an individual and which contain such reporting requirements as may be. Miscellaneous itemized deductions are those deductions that would have been subject to the 2 of adjusted gross income limitation. Examples of itemized deductions not subject to the 2 floor include costs related to fiduciary income tax returns and estate tax returns probate court costs and certain appraisal fees. The regulations will apply to tax years beginning on or after may 9 2014.

However deductions under section 67 e 1 continue to be deductible if they are costs that are incurred in connection with the administration of an estate or a non grantor trust that would not have been incurred if the property were. You must report the full amount of your winnings as income and claim your losses up to the amount of winnings as an itemized deduction.

Acct 426 Tax I Chapter 10 Flashcards Quizlet

Miscellaneous Tax Deductions To Claim On Your Tax Return

Tax Deductions For Individuals A Summary Everycrsreport Com

What Is The Standard Deduction Vs Itemized Deduction H R Block

Buffer A Smarter Way To Share On Social Media Backyard Views Garage Style Backyard

709 S Walnut Street Floor Trim Marysville Hardwood Floors

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Mending The Piggy Bank Budgeting Spreadsheet Budget Spreadsheet Budgeting Spreadsheet

Essay Reflection Goals And Graph By Wondering With Mrs Watto Create Student Accountability And Lifelong Writers The Essay Essay Writing Process Graphing

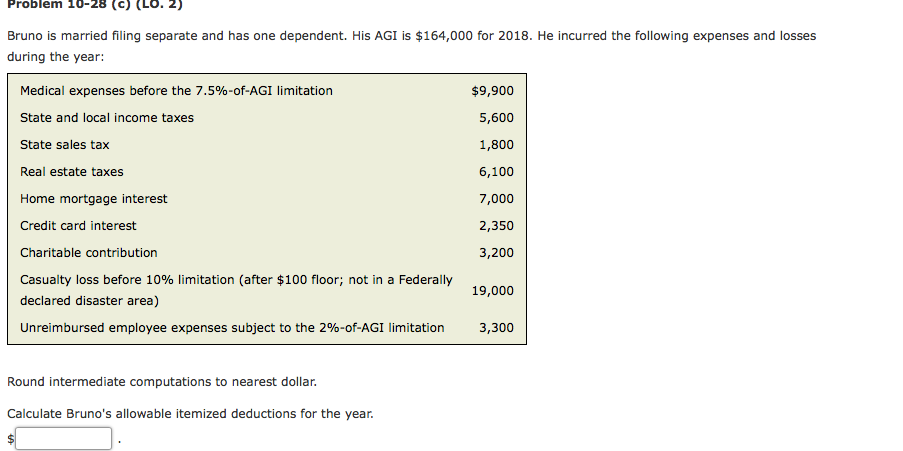

Solved Problem 10 28 C Lo 2 Bruno Is Married Filing Chegg Com

Great Ideas I Like The Subtleness Of These Suggestions It S Not Just About Putting A Giant Cow In 2020 Farm House Living Room Farmhouse Living Living Room Designs

Ppt Ch 09

Month To Months Residential Rental Agreement Free Printable Pdf Format Form Lease Agreement Free Printable Rental Agreement Templates Room Rental Agreement

Pin On Home Decoration Very Easy

Pin On Airbnb Tips

The Tax Benefit Of A Home Base Business At Endless Loweryourtaxableincome Home Based Business Successful Home Business Internet Business

Proceed With Caution When Making Pay Deductions For Salaried Employees

Consignment Agreement Google Search Consignment Shops Consignment Business Savvy

Income Tax Planning And Administration In Decedent S Estates Ppt Download

Do I Qualify For The 199a Qbi Deduction Myra

Acct321 Chapter 06

Notice Of Late Rent Free Printable Documents Late Rent Notice Rental Property Management Rent

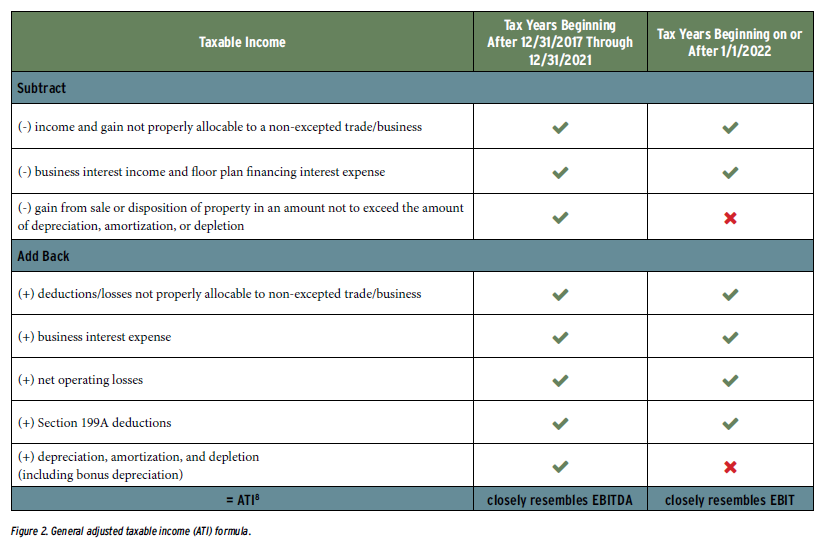

Part I The Graphic Guide To Section 163 J Tax Executive

What Home Buyers Need To Know When Mortgage Rates Rise Even Just A Fraction Mortgage Rates Best Mortgage Lenders Mortgage

Printable Sales Contract For Buying Subject To Template 2015 Real Estate Contract Real Estate Forms Contract Template

How To File An Illinois Sales Tax Return

Unit 1602 The Warwick The Unit Floor Plans Master Bath

Known Facts About Direct Admission In Top Mba College University Of Delhi College Names Mba

Office Depot Brand Time Cards With Deductions Weekly Monday Sunday Format 2 Sided 3 38 X 8 78 Manila Pack Of 100 Office Depot

Printable Sample Free Printable Rental Agreements Form Lease Agreement Rental Agreement Templates Room Rental Agreement

The 8 Most Important Questions To Ask Before Hiring Any Moving Company Redfin Real Time Realestate Diy Ctrealtor Plainvi Real Estate Hiring Movers Realty

14 Best Companies To Work For That Are Actually Making A Difference In The World Good Company Investment In India Company

Are Home Improvements Tax Deductible It Depends On Their Purpose Business Insider

It S Your Favorite Post Of The Week Time To Test Your Knowledge With An Mcq Leave A Comment With Your Answer And We Ll Let Yaeger Cpa Review Blog Cpa R

Pergola Front Porch In 2020 Pergola House Styles Front Porch

Should I Choose The Standardized Or Itemized Deductions And Answers To All Your Other Tax Questi With Images This Or That Questions Tax Questions Health Insurance Cost

Investment Fees Are Not Deductible But Borrow Fees Are Greentradertax

Unique Rental Application Form Free Xls Xlsformat Xlstemplates Xlstemplate Check More At H Rental Agreement Templates Lease Agreement Room Rental Agreement

Subject To Existing Liens Aka Sub 2 Real Estate Contract Download Now Real Estate Contract Real Estate Investing Positive Cash Flow

Free Printable Rental Agreement Elegant 11 Best Rental Agreements Images On Pinterest Rental Agreement Templates Lease Agreement Room Rental Agreement

Personal Property Rental Agreement Forms Property Rentals Direct Termination Of Lease Agr Lease Agreement Rental Agreement Templates Termination Of Tenancy

Listing 410 Glasgow Road Cary Nc 27511 House Bathtub Alcove Bathtub

:max_bytes(150000):strip_icc()/GettyImages-514211407-7890c9f9232844d1863ab073895a7c6f.jpg)

Non Accountable Plan Definition

:max_bytes(150000):strip_icc()/5-5c11282246e0fb0001e671f3.jpg)